24 January 2025

Atos, the natural daughter of the French State: two bond investments to avoid

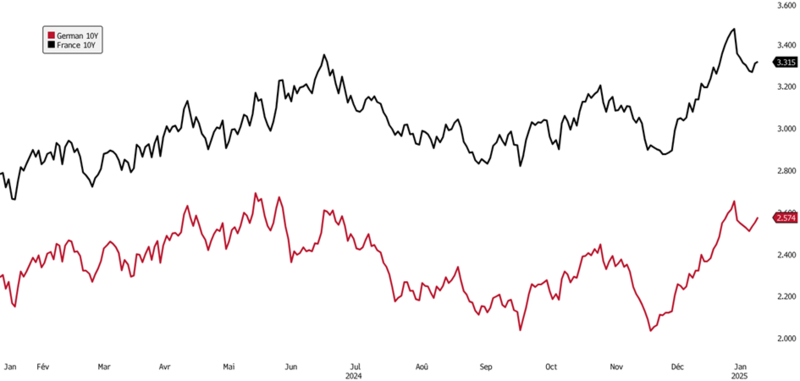

The 2025 bond market year begins as a continuation of 2024 in terms of volatility, as illustrated by the graph below showing German and French 10-year yields.

Sources : (Bloomberg, Octo Asset Management)

While some may view this widening as an attractive entry point to increase duration or acquire sovereign bonds, we believe that the massive financing needs of European states for the year are far from being met. Additionally, political interferences remain significant, ranging from initial trade negotiations with the U.S. to political hesitations and reversals in France and Germany.

Of course, if Eurozone countries only faced these challenges while benefiting from a strong economic and social environment, one might consider a 2.5–3% yield on a counter-cyclical issuer as sufficient in comparison to riskier assets like high-yield bonds or equities in the long term. However, this is far from the case. The current fiscal and balance sheet situation of European states does not allow us to consider such yields sufficient, especially for international investors who might also question the stability of the euro exchange rate.

As such, we will continue, for now, to prioritize corporate bonds, which have the added advantage of not being subject to potential rule changes mid-game, a temptation that governments could face in the coming years. The comments this week by Mr. Villeroy de Galhau about "mobilizing European savings" for investment purposes are an initial warning sign. In countries like France, Italy, or Spain, the doctrine often leans towards channeling large investment programs through the public sector. Mobilizing savings, in the language of a French technocrat, typically translates to taxes or redirecting savings toward state financing, rather than incentivizing direct investment.

Three main obstacles arise when it comes to this need for investment—both to revive the European economic engine and to secure sovereignty in the face of the U.S. and China in the decades ahead:

- A fundamental disagreement between Southern Europe (including France), which favors public financing, and Northern Europe, led by Germany, which prioritizes private financing.

- A lack of alignment of interests among Eurozone countries regarding sectors of activity, energy sources, regulations, or even societal priorities.

- A misalignment of interests between states that "mobilize" savings for their own investment priorities—often driven by purely political motives—and the interests of investors, particularly regarding time horizons, risk, and returns.

- A lack of reliability among states in managing and monitoring their investments and accounts, as evidenced by:

- France’s mismanagement of its 2024 budget, which includes an €11 billion overestimation of VAT revenues, as reported by Les Echos this week.

- The relatively poor track record of countries like France in terms of strategic investments. Examples include emblematic failures such as Atos (which we will revisit below), Areva, Bull, Thomson, and even the all-electric transition for personal transportation, whose limitations are already evident. Additionally, energy disputes between countries like France and Germany have often overshadowed successes, such as Airbus, whose glory days now feel distant.

Atos recently published its liquidity status as of the end of 2024, showing €2.2 billion in liquidity and seemingly reassuring debt reduction plans for investors. However, three points temper this optimism:

- Beyond the scope of accounting revisions or exceptional gains and losses in its history, the execution of the strategic plan underlying Atos's financial restructuring involves significant risks, making this €2 billion liquidity position insufficient as a safety buffer "a priori," as noted in our June 2022 report.

- Despite this restructuring, Atos will remain a loss-making company for years to come, both in terms of net income and free cash flow, which is not expected to turn positive before 2027 at the earliest. Recent debt instruments issued during this safeguard plan bear high interest rates, ranging from 9% for the 2029 bond to 13% for certain loans.

- Of the €2 billion liquidity position, only €40 million can genuinely be allocated toward improving the group's performance. The remainder includes €319 million from early payments by public clients, €240 million from the sale of Worldgrid in December, and €440 million from an undrawn revolving credit facility.

In short, we do not consider Atos to be out of the woods and will continue to avoid investing in its bonds for three key reasons:

- Lack of reliability in financial statements and management plans.

- A restructuring designed to benefit a few creditors, whose returns (10–13%) far exceed those of bondholders (9%).

- Strategic activities tied to the state and a strong political connection that create complex management, rife with conflicts of interest, rendering financial analysis unreliable and exposing investors to excessive risks.